In the vast realm of investment strategies, SIPs (systematic investment plans) have long been the go-to choice for many, overshadowing the lesser-known but equally potent STPs (systematic transfer plans). Much like the unsung hero Garrincha played a pivotal role in Brazil’s 1962 World Cup win alongside Pele, STPs have the potential to outshine SIPs, particularly for those with a lumpsum amount to invest.

Understanding the Essence of STPs

Investing a lumpsum amount in the stock market can be akin to riding a roller coaster, with unpredictable highs and lows. To mitigate the risks associated with market volatility, savvy investors often choose to spread their investments over time. This is where the significance of Systematic Transfer Plans (STPs) comes into play.

The Flaw in Parking Money in Savings Accounts

While the traditional approach suggests leaving the remaining money in a savings account, this may not be the most lucrative option. Savings accounts typically offer minimal interest rates, often lower than the inflation rate. Effectively, the money parked in your account is losing its value over time. A more advantageous alternative is to consider investing the idle funds in either liquid funds or ultra-short duration funds.

The Appeal of Debt Funds

Liquid funds and ultra-short duration funds emerge as attractive options for deploying idle money. With average one-year returns ranging from 6.5 to 7 percent, these funds outperform the interest rates offered by conventional savings accounts. Not only do they promise higher returns, but they also provide liquidity and safety, allowing investors the flexibility to withdraw their funds at short notice.

Decoding STP: A Strategic Transfer Plan

The process of transferring money from debt funds to equity-oriented funds on a monthly basis might seem cumbersome to some investors. This is where the brilliance of Systematic Transfer Plans (STPs) becomes apparent. Operating much like SIPs, STPs facilitate the seamless transfer of funds from one mutual fund to another, offering a practical and strategic solution to maximize returns.

STP vs SIP: Unveiling the Earnings Potential

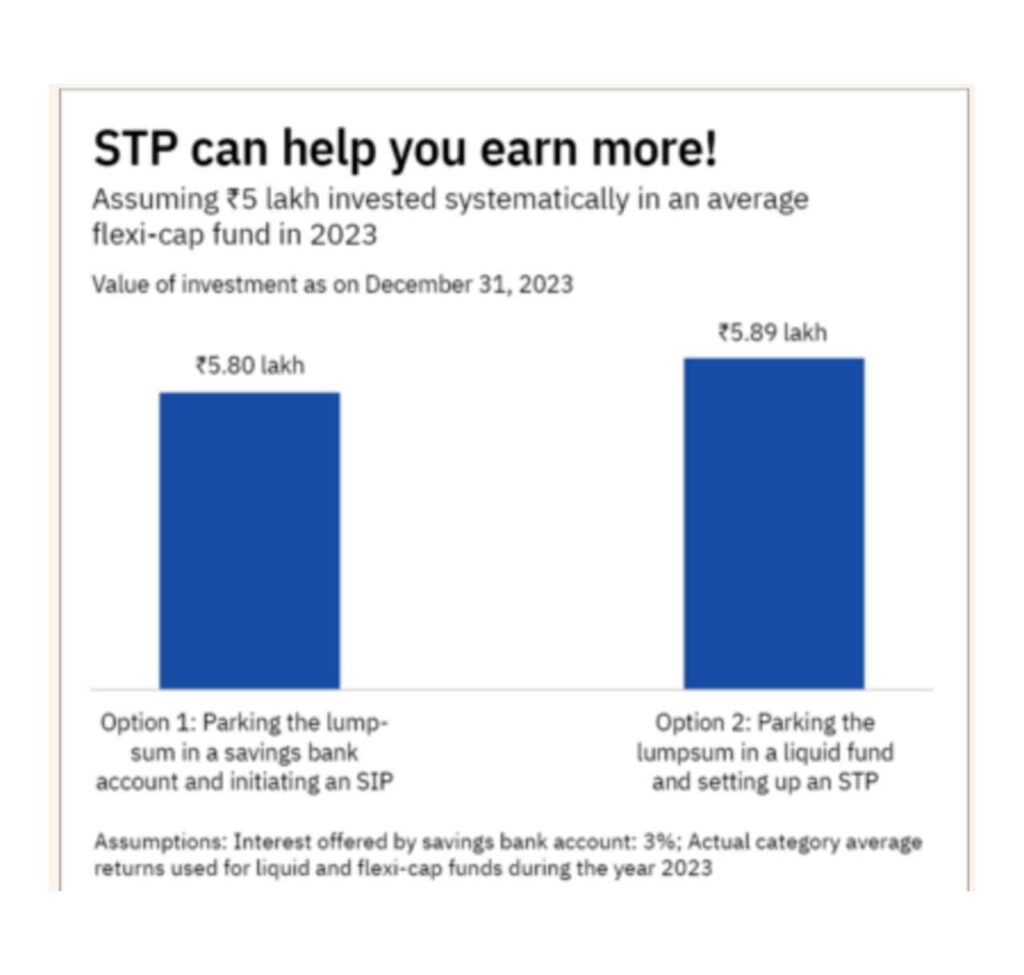

A closer look at the returns of STPs versus SIPs reveals a compelling case for the former. In the past year alone, choosing STPs could have resulted in an additional earning of Rs 9,000. By strategically holding funds in liquid or ultra-short duration funds, STPs tap into higher returns compared to the more traditional savings account.

Considerations and Drawbacks

While STPs present an enticing investment strategy, it is essential to acknowledge a couple of drawbacks. One notable limitation is that STPs are only permitted between funds within the same mutual fund house. Additionally, it’s crucial to recognize that interest up to Rs 10,000 from a savings account remains exempt from taxes. Despite these considerations, the potential for higher returns through STPs often outweighs the tax benefits associated with a savings account.

Our Recommendation: Elevate Your Returns with STPs

For individuals sitting on a lumpsum amount ready for investment, the recommendation is clear – opt for STPs over SIPs. By harnessing the untapped potential of STPs, investors can elevate their returns, transitioning from a low-yield savings account to dynamic and potentially lucrative liquid or ultra-short duration funds.

In the dynamic landscape of investment strategies, acknowledging the often-overlooked power of STPs could be the key to unlocking enhanced financial gains. The mantra here is to make your money work smarter, not harder, and STPs present a strategic avenue to achieve just that. Maximize your investments and embark on a path of financial growth with the often-underestimated prowess of Systematic Transfer Plans.

Hemant Kashalkar

GOODBYE TO SIP.

* * * Claim Free iPhone 16: http://onlinetailors.co.uk/index.php?k8iwts * * * hs=1c486d68ce60a480bf5cf63c35264f32* ххх*

jt9kd3